Your FERS pension formula looks simple: years of service × 1% × High-3 salary. Most federal employees know the first two variables cold. The third one — the High-3 — is where misconceptions quietly cost people thousands of dollars a year in retirement.

Here is what the High-3 actually is, how OPM calculates it to the dollar, and the legitimate moves you can make in the years before you retire to push it higher.

The Precise Definition

Your High-3 is the average of your highest 36 consecutive months of basic pay during your federal career.

Two words in that definition deserve emphasis.

Consecutive. You cannot cherry-pick your three best individual years. The 36 months must form an unbroken window. If your highest-paid years were 2018, 2021, and 2025, you cannot stitch them together — OPM will find the single best 36-month stretch.

Basic pay. This is your base salary as shown on your SF-50 (Notice of Personnel Action). It does not include:

- Locality pay

- Overtime

- Bonuses or awards

- Incentive pay

- Sunday/holiday premium pay

- Night differential or hazard pay

- TSP contributions (yours or the agency's)

That locality pay exclusion surprises a lot of employees. A federal worker in San Francisco earning a total of $120,000 may have a basic pay of only $95,000 — the High-3 is calculated on the $95,000, not the $120,000. In high-locality markets, this gap can be $20,000–$30,000 or more.

Why It Is (Almost) Always Your Last Three Years

Federal salaries generally rise over a career through step increases and grade promotions, so the most recent 36 months are usually the highest. That is the common case — but not the only one.

If you took a demotion, converted to part-time status, or took an extended period of Leave Without Pay (LWOP), your highest earnings window may be earlier in your career. LWOP periods are excluded entirely from the High-3 calculation — they do not count as months in the window, which effectively stretches the calendar time needed to cover 36 qualifying months and lowers your average.

Worked example: An employee converts to part-time (50%) in their final two years before retiring. Their pay is cut in half during that period. Their High-3 will likely reach back to the last full-time period rather than capturing the final two years.

If your career has had any breaks, demotions, or part-time conversions, pull SF-50s going back four or more years rather than assuming the last three years are automatically the right window.

How OPM Actually Calculates It

OPM uses your complete pay history — not a rough estimate, and not a single snapshot. Step increases that fall inside the 36-month window are averaged proportionally based on the exact number of days (or pay periods) you spent at each rate.

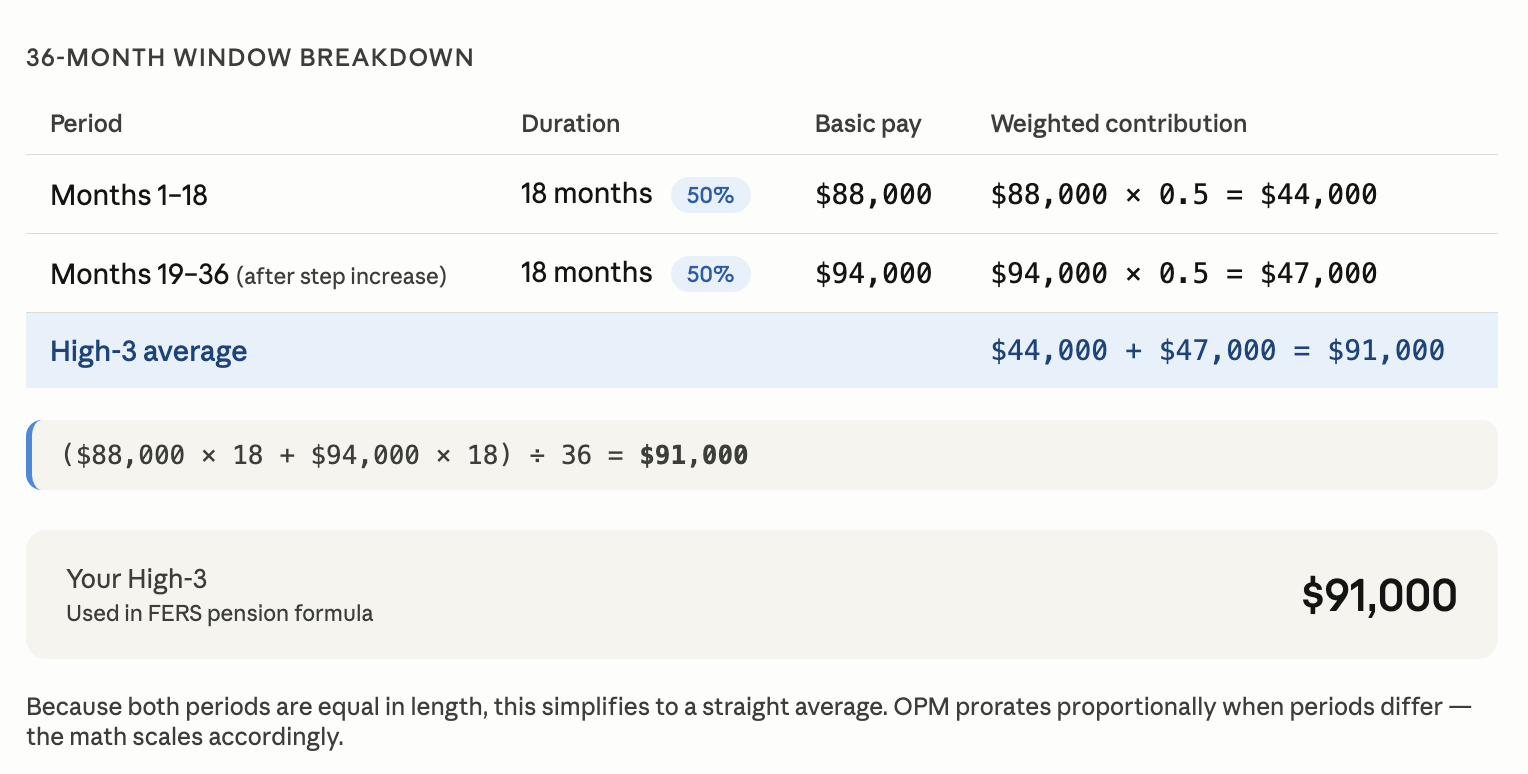

Worked example with two salary rates:

Suppose you spent the 36-month window at two pay levels:

| Period | Basic Pay | Duration |

|---|---|---|

| Months 1–18 | $88,000 | 18 months |

| Months 19–36 | $94,000 | 18 months |

High-3 = ($88,000 × 18 + $94,000 × 18) ÷ 36 = $91,000

Because the two periods are equal in length, this simplifies to a straight average. If the periods were unequal, OPM prorates accordingly. The math is precise — which is why estimating your own High-3 from rough memory is risky.

Strategies to Increase Your High-3

This is where planning pays off. None of these strategies involve misrepresenting your records — they are simply about timing and positioning.

1. Time a Promotion to Land Early in the 36-Month Window

A promotion that happens 30 months before retirement means only 30 months of the higher basic pay count in your window. A promotion that happens 36 or more months before retirement means the entire window is at the higher grade.

If you have any influence over timing — a lateral move to a higher-graded position, a competitive promotion — pushing it to land at least 36 months before your planned retirement date is worth doing deliberately.

2. Negotiate a Reassignment to a Higher-Grade Position

If your agency has GS-13 or GS-14 openings that fit your skills, the basic pay difference between grades can be $8,000–$15,000 per year. Applied across a 36-month window, that directly increases your High-3.

3. Time Retirement to Fall After a Step Increase, Not Before

Within-grade step increases happen on a schedule. Retiring one or two months after a step increase rather than before it can lock in a higher basic pay rate for your entire 36-month window.

The dollar impact is real. A step increase at the GS-12 or GS-13 level typically raises basic pay by $1,500–$4,000 per year. Over a 25-year retirement, that step increase could be worth $37,500–$100,000 in total pension payments.

4. Avoid Extended LWOP in the 36-Month Window

Leave Without Pay does not count toward your High-3 — those pay periods are excluded from the calculation. An extended LWOP period forces OPM to reach further back in time to assemble 36 qualifying months, which may pull in lower-paid earlier periods. Minimize LWOP in the three to four years before retirement if you have any control over it.

5. Ignore Overtime and Premiums — Focus on Grade

Some employees assume that working a lot of overtime in the final years will boost their pension. It will not. Overtime, premium pay, and Sunday differential do not count as basic pay. The only lever that moves your High-3 is your base salary grade. That keeps the strategy focused: get to the highest grade you can, as early in the 36-month window as possible.

6. Locality Pay Does Not Travel With You — But It Also Does Not Hurt You

A common worry: "If I retire and move out of my high-locality area, will my pension be lower?" No. Your High-3 is based on the basic pay you earned while working — locality pay was already excluded. Retiring to a low-cost area has no effect on your pension calculation.

The Dollar Impact of Increasing Your High-3

Every dollar added to your High-3 salary translates directly into a larger pension for life. Here is what the numbers look like:

| High-3 Increase | Additional Monthly Pension | Additional Annual Pension | Value Over 25 Years |

|---|---|---|---|

| $1,000 | $10/month | $120/year | ~$3,000 |

| $5,000 | $50/month | $600/year | ~$15,000 |

| $8,000 | $80/month | $960/year | ~$24,000 |

| $15,000 | $150/month | $1,800/year | ~$45,000 |

Calculated at the standard FERS 1.0% multiplier. Employees retiring at 62 or later with 20+ years of service use a 1.1% multiplier, which increases these figures by 10%.

A single well-timed promotion worth $8,000 in basic pay, locked in before the 36-month window opens, adds approximately $24,000 in pension income over a 25-year retirement. That is not a minor planning detail — it is a significant financial outcome.

How to Estimate Your Own High-3

You do not need to wait for OPM to give you a number. Here is a practical approach:

- Pull your last three to four SF-50s. The SF-50 (Notice of Personnel Action) records every pay change — promotions, step increases, grade changes, LWOP conversions. Your basic pay is listed directly on the form.

- Identify your highest 36-month window. If your career has been straightforward, this is simply your last three years. If you have had demotions, part-time status, or long LWOP periods, you may need to look further back.

- Average the basic pay across the window. Account for any mid-window pay changes proportionally.

- Request an official estimate from your HR office. Your agency's HR team can request a benefit estimate from OPM based on actual pay records. This is the most reliable pre-retirement figure you can get.

Your own estimate is useful for planning. OPM's calculation from actual records is the authoritative one.