If you’re a federal employee trying to figure out your retirement system, you’re not alone. The difference between CSRS and FERS isn’t just academic—it directly affects how much you’ll receive in retirement, when you can retire, and how much responsibility falls on you to save.

Let’s break it down clearly.

⸻

A Quick History: Why There Are Two Systems

The Civil Service Retirement System (CSRS) was the original retirement plan for federal employees, established long before Social Security became widespread.

That changed in the 1980s.

- Hired before 1984? You’re almost certainly under CSRS

- Hired between 1984–1986? You may have had a choice between CSRS and FERS

- Hired January 1, 1987 or later? You’re under FERS (with rare exceptions)

FERS (Federal Employees Retirement System) was designed to align federal benefits more closely with the private sector—meaning a smaller pension, but added Social Security and employer retirement contributions.

⸻

The Big Picture: CSRS vs FERS at a Glance

Here’s the high-level comparison most people are looking for:

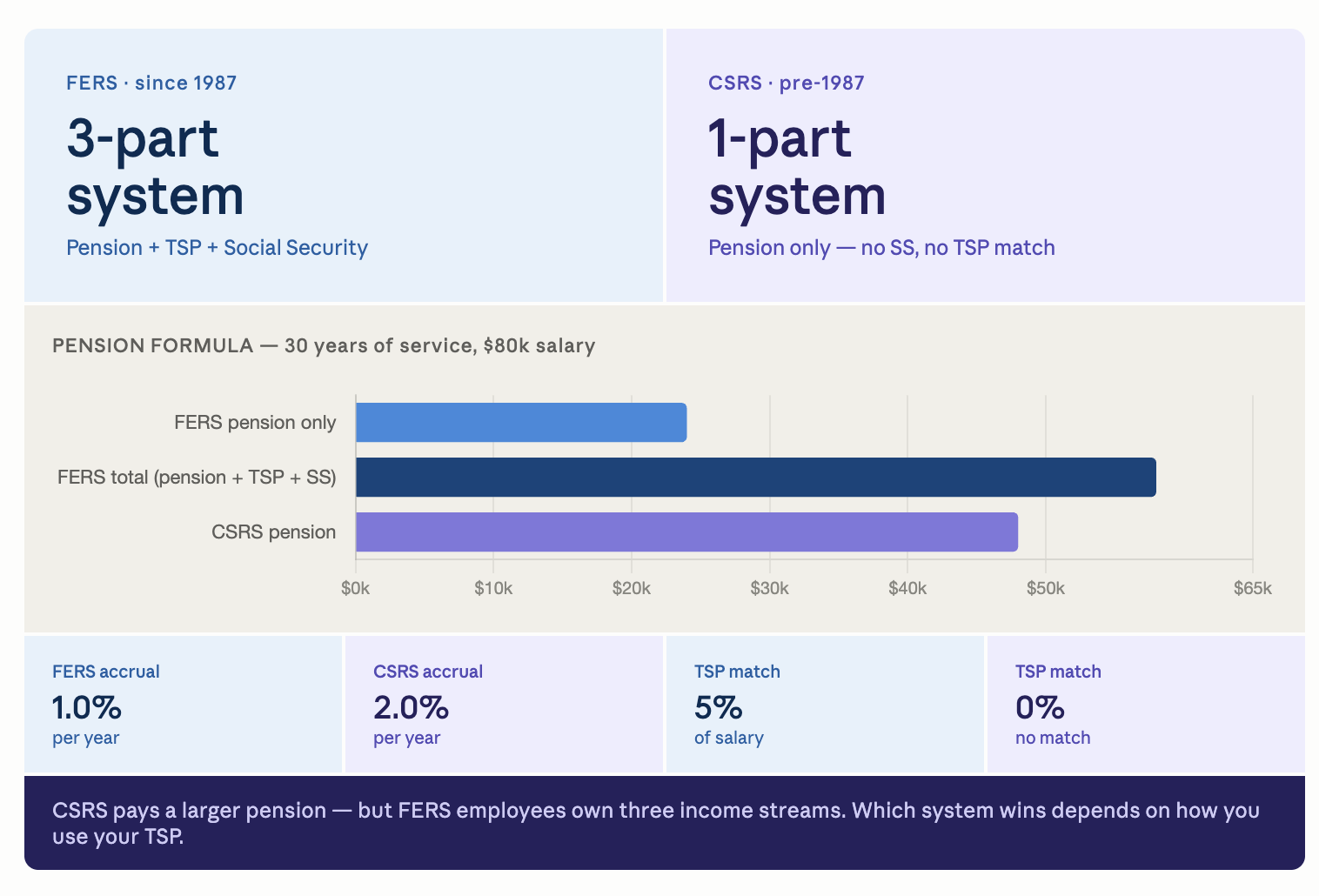

Feature CSRS FERS Pension formula More generous (up to ~56% at 30 years) Less generous (~30–33% at 30 years) Social Security Typically none Full participation TSP match No match Up to 5% agency contribution Retirement age Earlier (as low as 55) Based on MRA (55–57) COLA Full inflation Reduced inflation adjustments FERS Supplement Not applicable Yes (until age 62)

At a glance: CSRS leans on a strong pension, while FERS spreads benefits across pension + Social Security + TSP.

⸻

CSRS Offset: The Hybrid Many People Miss

There’s a third category that often causes confusion: CSRS Offset.

Who it applies to

CSRS Offset typically includes employees who:

- Started under CSRS

- Left federal service

- Came back after 1983 into a position covered by Social Security

How it works

- While working, you pay into both CSRS and Social Security

- Your pension is calculated like CSRS

- At age 62, your CSRS pension is reduced (offset) by the portion of Social Security you earned during federal service

In plain terms: you don’t lose money—but your income is split between a smaller pension + Social Security benefit.

⸻

Pension Formula: Where the Biggest Difference Shows Up

This is where CSRS and FERS diverge the most.

CSRS Formula (Tiered and Generous)

CSRS uses a stepped formula:

- 1.5% × first 5 years

- 1.75% × next 5 years

- 2.0% × all remaining years

Example: 30 Years of Service

- First 5 years: 7.5%

- Next 5 years: 8.75%

- Remaining 20 years: 40%

Total = 56.25% of your High-3 salary

If your High-3 is $100,000:

- Annual pension ≈ $56,250

⸻

FERS Formula (Simpler, Lower)

FERS uses a flat rate:

- 1.0% × years of service × High-3

- Or 1.1% if you retire at age 62+ with 20+ years

Example: 30 Years of Service

- Standard: 30% of High-3

- With age 62 boost: 33%

If your High-3 is $100,000:

- Annual pension ≈ $30,000–$33,000

⸻

What This Means

CSRS pensions are significantly larger. But that’s only part of the story—because FERS includes other income streams.

⸻

Social Security: The Defining Difference

CSRS

- Most CSRS employees do not pay into Social Security

- They typically do not receive Social Security benefits from federal service

- If they have outside work, benefits may be reduced due to WEP/GPO rules

FERS

- You pay full Social Security taxes

- You receive full Social Security benefits

This is one of the biggest structural differences between the systems.

⸻

TSP Matching: Free Money vs None

CSRS

- You can contribute to the Thrift Savings Plan (TSP)

- But your agency does not match contributions

FERS

You get:

- 1% automatic contribution (even if you contribute nothing)

- Matching contributions up to 4%

Breakdown:

- 100% match on first 3%

- 50% match on next 2%

If you contribute 5%:

- You receive the full 5% agency contribution

This is a major advantage—especially over a full career.

⸻

Retirement Eligibility

CSRS

- Age 55 with 30 years

- Age 60 with 20 years

- Age 62 with 5 years

FERS

- Minimum Retirement Age (MRA: 55–57 depending on birth year) with 30 years

- Age 60 with 20 years

- Age 62 with 5 years

- MRA + 10 option (reduced benefit)

FERS generally requires working longer for full benefits.

⸻

COLA: How Your Pension Keeps Up With Inflation

CSRS

- Full Cost-of-Living Adjustment (COLA)

- Tracks inflation (CPI) exactly

FERS

- Reduced COLA:

- If CPI < 2% → no reduction

- If CPI 2–3% → capped at 2%

- If CPI > 2% → reduced by 1%

Over a long retirement, this difference compounds significantly.

⸻

The FERS Supplement

FERS includes something CSRS does not: the FERS Supplement.

- Paid from retirement until age 62

- Designed to “bridge the gap” until Social Security begins

- Based on your years of FERS service

CSRS doesn’t have this because it doesn’t rely on Social Security.

⸻

Which System Is More Generous?

This is the question everyone wants answered—and the honest answer is: it depends on how you use FERS.

CSRS Advantages

- Larger pension (often nearly double FERS)

- Full inflation protection (COLA)

- Earlier retirement options

FERS Advantages

- Social Security income

- TSP matching (significant over time)

- More portable and flexible

The Reality

- If you don’t contribute much to TSP, CSRS is usually more generous

- If you maximize TSP contributions and invest well, FERS can match—or even exceed—CSRS total retirement income

FERS shifts more responsibility onto you. That’s the tradeoff.

⸻

Decision Tree: Which System Are You In?

If you’re unsure, start here:

- When were you first hired into federal service?

- Before 1984 → Go to #2

- 1984–1986 → You may have chosen → Check your SF-50

- 1987 or later → You’re FERS

- Did you leave federal service and return after 1983?

- Yes → You may be CSRS Offset

- No → You’re likely CSRS

- Still unsure?

- Check your SF-50 (Notification of Personnel Action)

- Look for retirement coverage code:

- “CSRS”

- “CSRS Offset”

- “FERS”

⸻

Final Thoughts

CSRS and FERS aren’t just different plans—they reflect two completely different philosophies of retirement. One leans heavily on a guaranteed pension. The other blends pension, Social Security, and personal savings.

Knowing which system you’re in is step one. Knowing how to optimize it is what actually determines your retirement outcome.

Want to see how your benefits add up across pension, Social Security, and TSP? Try the free calculator at https://fedsage.com and get a clear picture of your retirement in minutes.