The Three-Legged Stool — and Why the Legs Talk to Each Other

If you've spent any time reading about FERS retirement, you've heard the three-legged stool: your pension (the FERS basic annuity), your Thrift Savings Plan, and Social Security. What most explanations gloss over is that these three legs aren't independent. When you pull on one, the others shift. That's especially true when it comes to deciding when to claim Social Security.

For a private-sector worker, the Social Security timing decision is mostly a math problem about longevity and cash flow. For a FERS employee, it's a math problem that also involves your supplement, your pension start date, and how aggressively you want to draw down your TSP. Getting this right can be worth tens of thousands of dollars over a 25-year retirement.

Takeaway: Before you search for generic Social Security advice, make sure the source understands that FERS employees have a fourth income source — the FERS Supplement — that changes the calculus entirely.

The Three Claiming Ages: What the Numbers Actually Mean

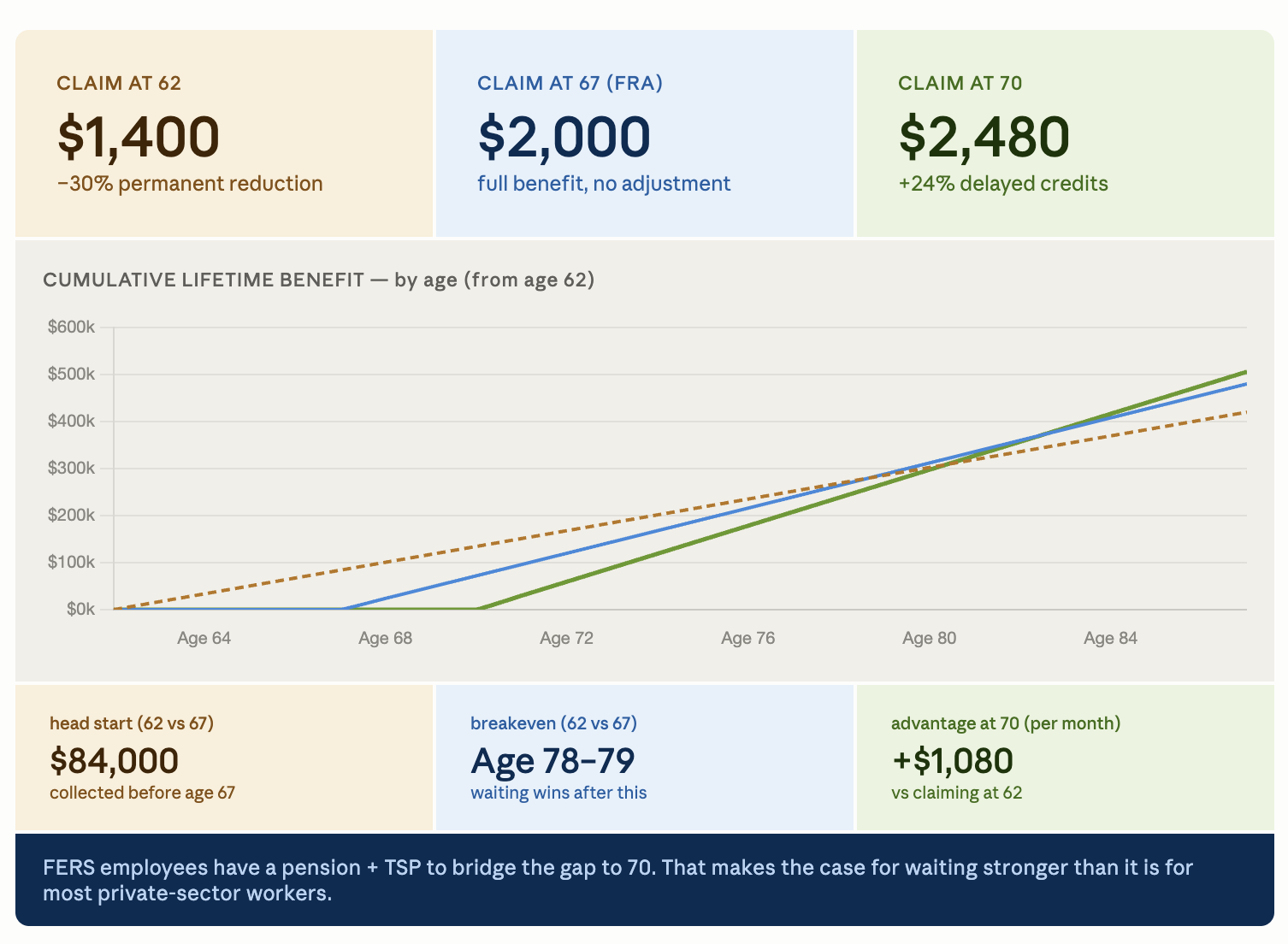

Social Security gives you a choice: claim early and accept a permanent reduction, wait for your Full Retirement Age (FRA) and get your full benefit, or delay past FRA and earn bonus credits. Here's how that works for someone born in 1960 or later, whose FRA is age 67.

Claiming at 62 (the earliest possible age) locks in a permanent reduction of up to 30% below your FRA benefit. That reduction never goes away — it applies to every check you receive for the rest of your life, and to any survivor benefit your spouse may later collect.

Claiming at your FRA of 67 gives you 100% of your calculated benefit — the number Social Security shows you on your statement.

Claiming at 70 earns you Delayed Retirement Credits of 8% per year for each year you wait past FRA. That's a cumulative 24% increase over your FRA benefit if you wait all three years from 67 to 70. After age 70, there is no further increase, so there is no reason to wait beyond your 70th birthday.

| Claiming Age | Adjustment (FRA = 67) | Example Monthly Benefit |

|---|---|---|

| 62 | −30% | $1,400 |

| 63 | −25% | $1,500 |

| 64 | −20% | $1,600 |

| 65 | −13.3% | $1,733 |

| 66 | −6.7% | $1,867 |

| 67 (FRA) | No adjustment | $2,000 |

| 68 | +8% | $2,160 |

| 69 | +16% | $2,320 |

| 70 | +24% | $2,480 |

Assumes a $2,000/month benefit at FRA. Your actual benefit will differ.

Takeaway: The difference between claiming at 62 and waiting until 70 is $1,080 per month in this example — for life. Before you lock in the early rate, make sure you understand what you're trading away.

The Breakeven Calculation: When Does Waiting Pay Off?

The classic breakeven question is: at what age does the larger delayed benefit catch up to all the payments you missed by waiting?

Here's a worked example. Suppose your FRA benefit is $2,000 per month at age 67.

Option A — Claim at 62: You receive $1,400/month. Over five years (ages 62–67), you collect $84,000 before your FRA-claiming counterpart gets a single check.

Option B — Claim at 67: You receive $2,000/month, which is $600 more per month than Option A.

To find the breakeven, divide the head start ($84,000) by the monthly advantage ($600): that's 140 months, or about 11.7 years. Add that to age 67 and you get roughly age 78–79 as the crossover point.

If you live past 79, Option B wins in total lifetime dollars. If you live past 70 and claim at 70 instead of 67, the crossover against age-62 claiming is roughly age 80–81 — and the monthly advantage thereafter is $1,080/month, compounding over years.

The Social Security Administration reports that the average 62-year-old today can expect to live into their mid-to-late 80s. For a married couple, the odds that at least one spouse reaches 85 are well above 70%. Longevity risk — the risk of outliving your money — is the primary case for delayed claiming.

Takeaway: If your health is good and you have other income to bridge the gap, the breakeven math increasingly favors waiting. The question is whether you can wait — which brings us to the supplement.

The FERS Supplement: The Hidden Factor That Rewrites the Decision

The FERS Supplement is one of the most misunderstood pieces of federal retirement. It is not Social Security. It is not your pension. It is a separate benefit paid by OPM to FERS employees who retire before age 62, designed to approximate what your Social Security benefit will eventually be — giving you income during the years you can't yet claim the real thing.

Two rules govern the supplement that every FERS retiree must internalize:

Rule 1: The FERS Supplement stops when you turn 62. Period. It doesn't matter if you've claimed Social Security or not. The day you turn 62, the supplement is gone.

Rule 2: The supplement is subject to an earnings test while you receive it. If you earn more than the annual limit from wages (the same threshold that applies to early Social Security claimants), your supplement is reduced.

This creates three distinct scenarios once you reach 62.

Scenario A — You claim Social Security at 62. The supplement ends and Social Security begins in the same month. There is no income gap, but you lock in that permanent 30% reduction on your SS benefit for the rest of your life.

Scenario B — You delay Social Security past 62. The supplement ends at 62, and Social Security doesn't start until you choose to claim it at 65, 67, or 70. That gap — anywhere from three to eight years — is an income gap you must fill from somewhere. The most common source is TSP withdrawals.

Scenario C — You don't receive the supplement at all. FERS employees who retire at or after age 62, or who retire on a MRA+10 (Minimum Retirement Age plus 10 years of service) annuity, don't receive the supplement. For these employees, the Social Security timing decision is more straightforward.

Bridging the Gap with TSP

If you delay Social Security past 62, your TSP becomes your bridge. Suppose your FERS Supplement was $1,200/month and you plan to delay SS until 67. You'll need to replace five years of that income — about $72,000 in total — from your TSP. At a 4% annual withdrawal rate, you'd need roughly $180,000 in TSP assets just to cover that gap without touching principal. Most FERS retirees have significantly more than that, but it's worth running the numbers for your specific balance before committing to a delay strategy.

Takeaway: The supplement's end at 62 is not optional and not negotiable. Plan for that cliff well in advance, and make sure your TSP withdrawal strategy accounts for it if you intend to delay Social Security.

The Earnings Test: A Trap for Those Who Retire Young and Go Back to Work

If you claim Social Security before your FRA and continue to work — or return to work — Social Security will reduce your benefit if your wages exceed the annual earnings limit. For 2025, that threshold is approximately $22,320 per year. For every $2 you earn above that limit, Social Security withholds $1 in benefits.

For example, if your Social Security benefit is $1,400/month ($16,800/year) and you earn $42,320 in wages, you've exceeded the limit by $20,000. Social Security withholds $10,000 — roughly six months of your checks.

The withheld money is not simply lost. After you reach FRA, Social Security recalculates your benefit upward to credit you for the months it withheld. But the recalculation is complex, and the timing of the catch-up is unpredictable. For federal employees doing part-time consulting or a second career in their early 60s, the earnings test is a strong argument against claiming Social Security until you've fully stopped working.

Takeaway: If there's any chance you'll earn more than roughly $22,000/year from wages after claiming, seriously reconsider claiming early. The reduction is real and the recovery is slow.

Spousal Benefits: A Brief But Important Note

If you are married, your Social Security claiming decision affects more than just your own benefit. A lower-earning spouse may be entitled to a spousal benefit equal to up to 50% of your FRA benefit — and they cannot receive that full spousal benefit until you have claimed. Additionally, when one spouse dies, the survivor steps up to the higher of the two benefits. Claiming early permanently reduces that survivor benefit, which can significantly harm a surviving spouse who lives for many years after.

For couples with a meaningful earnings gap, the higher earner delaying to 70 is often the most powerful longevity insurance available within the Social Security system.

WEP: What CSRS Employees (and Some FERS Employees) Need to Know

If you spent part of your career under CSRS — the older Civil Service Retirement System — or if you have a pension from any job that didn't withhold Social Security taxes, you may be subject to the Windfall Elimination Provision (WEP).

WEP modifies the formula Social Security uses to calculate your benefit, reducing the amount you receive. The reduction can be as much as half of your non-covered pension amount, capped at approximately $587/month in 2025. For a CSRS retiree with a substantial pension, this reduction can be significant — potentially $400 to $587/month less than a purely Social Security-covered worker would receive.

Pure FERS employees who spent their entire career under FERS are generally not affected by WEP, because FERS employment is covered by Social Security. However, if you had earlier CSRS service, a state or local government pension, or foreign pension income from non-covered employment, check your WEP status before assuming your Social Security statement reflects what you'll actually receive.

Takeaway: If any part of your career was under CSRS or another non-SS-covered pension, budget for WEP before you finalize your retirement income projections.

A Decision Framework: Questions to Ask Before You Choose

Deciding when to claim Social Security is not a one-size-fits-all problem. Here is a practical set of questions to work through with your financial planner or a federal retirement specialist.

What is your health and family longevity? If your parents and grandparents lived into their late 80s and your own health is good, the math favors delay. If you have serious health concerns, earlier claiming may make sense.

Do you receive the FERS Supplement, and have you planned for it ending at 62? If you retire before 62, make sure your budget accounts for the income cliff, and decide whether you want Social Security to fill it immediately or whether you'd rather use TSP to bridge a longer delay.

Can your TSP and pension cover your needs from 62 to 67 or 70? Run the numbers. Your FERS pension is your floor. Your TSP is your bridge. Social Security is your long-term hedge against inflation and longevity.

Will you work after retirement? If yes and your wages will exceed ~$22,320/year, don't claim Social Security before FRA.

Does your spouse have a meaningfully lower benefit? If so, your decision about when to claim affects their lifetime security. The higher earner delaying to 70 protects a surviving spouse for potentially decades.

Are you subject to WEP? If CSRS service is in your history, get a WEP estimate before finalizing your projections.

What is your primary risk? If you're most worried about running out of money in your 80s, delay. If you're most worried about cash flow in your early 60s, the supplement-to-SS bridge may point toward claiming earlier and adjusting TSP accordingly.